All Categories

Featured

Table of Contents

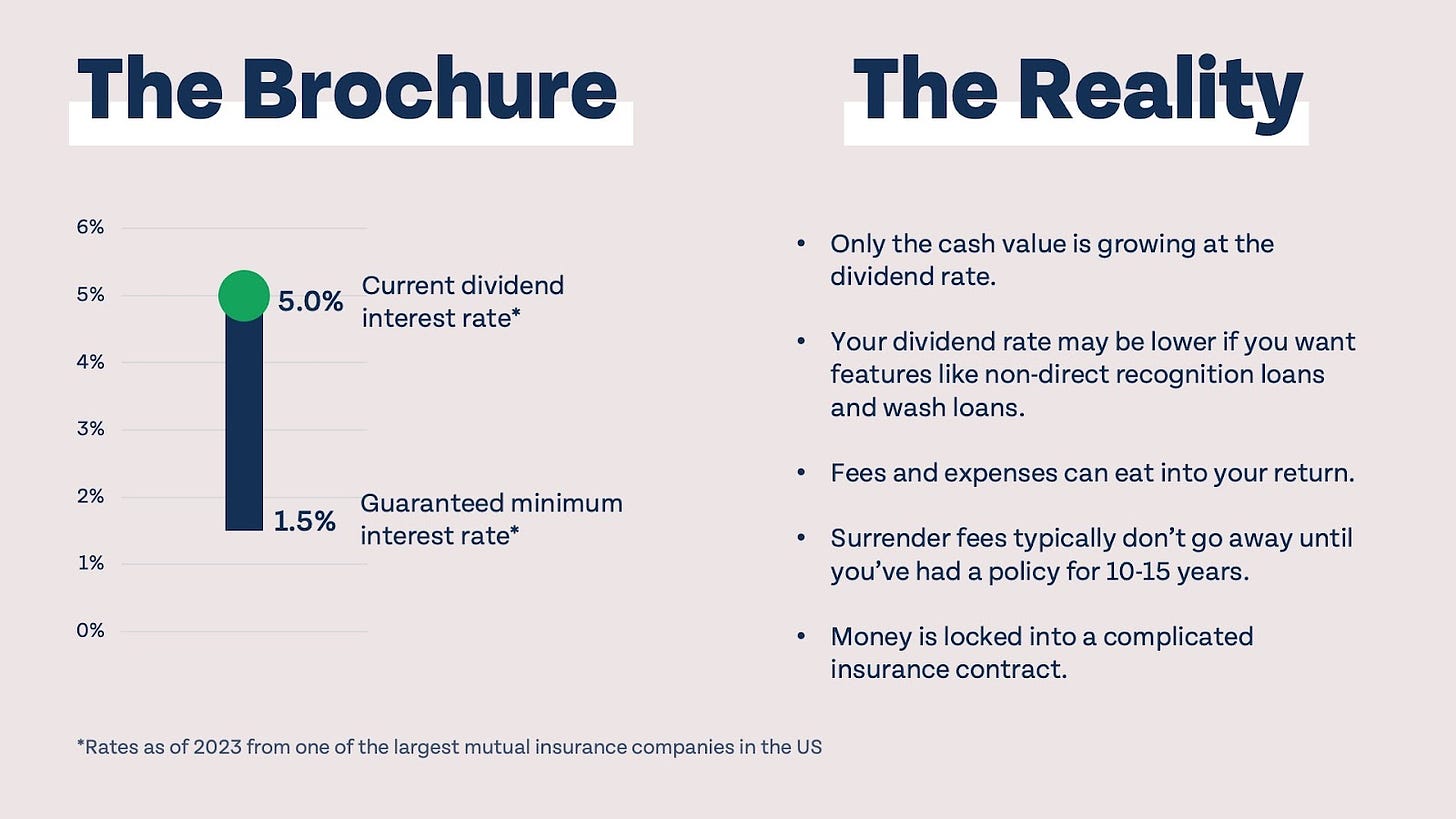

The drawbacks of unlimited financial are often ignored or otherwise discussed in all (much of the details readily available regarding this principle is from insurance coverage agents, which might be a little biased). Just the cash money value is expanding at the reward rate. You additionally need to pay for the price of insurance policy, charges, and expenditures.

Every irreversible life insurance policy is different, but it's clear somebody's total return on every buck invested on an insurance product might not be anywhere close to the reward rate for the policy.

Infinite Banking Agents

To provide a very basic and hypothetical example, allow's assume someone is able to earn 3%, generally, for every single dollar they invest in an "unlimited banking" insurance coverage product (besides expenses and fees). This is double the approximated return of whole life insurance policy from Customer News of 1.5%. If we think those bucks would certainly be subject to 50% in tax obligations amount to if not in the insurance coverage product, the tax-adjusted price of return might be 4.5%.

We assume greater than ordinary returns on the entire life item and an extremely high tax rate on dollars not take into the plan (that makes the insurance coverage item look far better). The reality for many people might be even worse. This pales in comparison to the long-lasting return of the S&P 500 of over 10%.

Infinite financial is a fantastic product for representatives that offer insurance policy, but might not be optimum when compared to the less expensive alternatives (without sales individuals gaining fat commissions). Below's a break down of several of the other supposed advantages of boundless banking and why they may not be all they're split up to be.

Infinite Banking Forum

At the end of the day you are buying an insurance item. We enjoy the protection that insurance policy uses, which can be acquired much less expensively from an affordable term life insurance policy plan. Overdue finances from the plan might additionally reduce your fatality advantage, decreasing an additional degree of protection in the policy.

The concept only works when you not just pay the significant costs, but use extra cash money to acquire paid-up enhancements. The chance cost of every one of those bucks is significant extremely so when you could rather be buying a Roth Individual Retirement Account, HSA, or 401(k). Even when compared to a taxed investment account and even a cost savings account, infinite financial might not offer equivalent returns (contrasted to investing) and equivalent liquidity, gain access to, and low/no cost framework (compared to a high-yield interest-bearing accounts).

With the increase of TikTok as an information-sharing platform, financial recommendations and techniques have found an unique method of spreading. One such strategy that has actually been making the rounds is the boundless banking principle, or IBC for short, amassing recommendations from stars like rap artist Waka Flocka Fire. Nonetheless, while the approach is currently prominent, its origins map back to the 1980s when economic expert Nelson Nash introduced it to the globe.

Within these plans, the money value expands based upon a rate set by the insurance company. When a substantial cash value accumulates, insurance holders can get a cash value financing. These fundings vary from standard ones, with life insurance policy offering as collateral, implying one might shed their coverage if borrowing exceedingly without sufficient cash money worth to support the insurance coverage expenses.

Life Insurance Be Your Own Bank

And while the allure of these policies is evident, there are innate limitations and dangers, demanding attentive money value monitoring. The strategy's authenticity isn't black and white. For high-net-worth individuals or service owners, particularly those utilizing methods like company-owned life insurance policy (COLI), the advantages of tax obligation breaks and substance development could be appealing.

The appeal of boundless banking doesn't negate its difficulties: Cost: The foundational need, a permanent life insurance policy plan, is more expensive than its term counterparts. Eligibility: Not everyone certifies for entire life insurance coverage due to rigorous underwriting procedures that can omit those with specific health and wellness or way of life conditions. Complexity and risk: The detailed nature of IBC, coupled with its threats, might hinder numerous, particularly when less complex and much less high-risk alternatives are available.

Designating around 10% of your monthly income to the policy is simply not practical for most individuals. Making use of life insurance coverage as an investment and liquidity resource requires discipline and tracking of plan cash value. Speak with a monetary expert to determine if limitless financial lines up with your concerns. Part of what you check out below is simply a reiteration of what has already been said over.

So prior to you obtain into a scenario you're not planned for, recognize the complying with initially: Although the idea is frequently marketed therefore, you're not really taking a funding from on your own - life insurance infinite banking. If that were the case, you would not have to settle it. Rather, you're borrowing from the insurance policy company and have to repay it with interest

Infinite Banking State Farm

Some social media blog posts suggest using cash money worth from whole life insurance to pay down credit card financial obligation. When you pay back the loan, a portion of that passion goes to the insurance policy business.

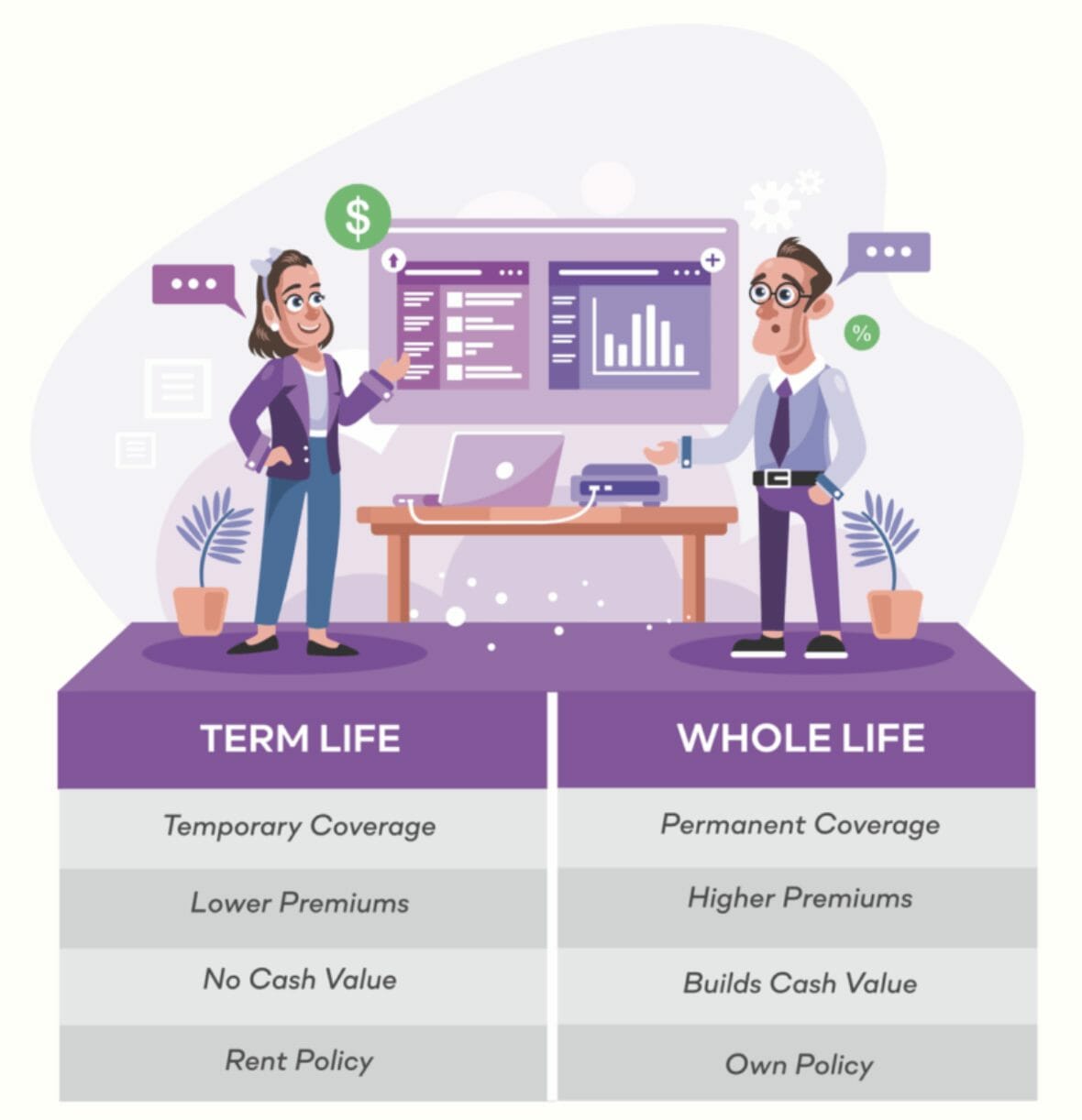

For the very first a number of years, you'll be settling the compensation. This makes it very hard for your plan to build up worth throughout this moment. Entire life insurance policy prices 5 to 15 times extra than term insurance coverage. Most individuals just can not manage it. So, unless you can manage to pay a few to a number of hundred bucks for the next years or more, IBC won't benefit you.

If you call for life insurance coverage, right here are some important ideas to think about: Consider term life insurance policy. Make certain to go shopping around for the best price.

Unlimited banking is not a product and services provided by a details establishment. Unlimited financial is a technique in which you buy a life insurance coverage policy that builds up interest-earning cash worth and secure financings versus it, "borrowing from yourself" as a resource of capital. After that ultimately pay back the finance and begin the cycle around once again.

Pay plan costs, a portion of which builds cash money value. Take a funding out against the policy's cash money worth, tax-free. If you use this principle as intended, you're taking cash out of your life insurance coverage plan to purchase everything you 'd need for the remainder of your life.

{kind=link}

Table of Contents

Latest Posts

Cash Flow Banking Strategy

Is Bank On Yourself Legitimate

Becoming Your Own Bank

More

Latest Posts

Cash Flow Banking Strategy

Is Bank On Yourself Legitimate

Becoming Your Own Bank